Can 401(k) reduce my taxes? Learn how

April 1, 2025

When planning for retirement, one of the most effective tools available to U.S. employees and employers is the 401(k) plan. Not only does a 401(k) help build a nest egg for the golden years, but it also provides tangible tax benefits.

Here’s a detailed guide on how this retirement savings plan can help reduce taxes for individuals and businesses alike.

What Is a 401(k) Plan?

A 401(k) is a savings plan for retirement. It is employer-sponsored and it is designed to allow employees to save a part of their income for when they retire.

Contributions are often deducted directly from an employee’s paycheck and can be made on a pre-tax (Traditional 401(k)) or post-tax (Roth 401(k)) basis, depending on the plan type chosen. Many employers also offer matching contributions, providing additional incentives for employees to participate. It is a defined contribution plan, which means that there is a limit set to how much an employee and an employer can contribute to the 401(k).

For 2024, the combined contributions of the employer and the employee cannot exceed US$69,000 and it will be US$70,000 for 2025. The idea behind this plan is to encourage long-term savings by providing tax savings and investment options. It is popular because of its dual benefit of promoting retirement security and offering tax incentives that can have a significant impact on a person’s personal and financial well-being.

Can a 401(k) Reduce Taxes?

The short answer is yes, and here’s how:

For Employees

- Reduction of Taxable Income

The income you have earned before paying the tax is used to contribute money to a Traditional 401(k). This can lower your taxable income. For example, if your annual income is $80,000 and you put in $10,000 to your 401(k), you are only taxed on $70,000. This immediate reduction can lead to substantial savings, particularly for those in higher tax brackets.

- Tax-Deferred Growth

Investments made within your Traditional 401(k) grow tax-deferred. This means you don’t pay taxes on dividends, interest, or capital gains until you withdraw funds during retirement. The longer your money remains in the account, the more it benefits from compounding without the drag of taxes.

- Roth 401(k) Advantages

Roth 401(k) is also a retirement savings plan just like the traditional 401(k). Although Roth 401(k) contributions are made with post-tax dollars and don’t reduce taxable income in the present, qualified withdrawals in retirement are tax-free.

This can be really beneficial for people who think that they will be in a higher tax bracket when they are about to retire.

- Catch-Up Contributions

The IRS sets annual contribution limits for 401(k) plans, which for 2024 is $23,000 for individuals under 50 and an additional $7,500 for those aged 50 or older.

This additional catch-up amount set for people aged 50 and older not only boosts retirement savings but also provides more opportunities to reduce taxable income or invest for future tax-free withdrawals, depending on the type of 401(k).

Moreover, one must note that contributing the maximum allowed amount not only accelerates retirement savings but also maximizes the tax benefits available.

For Employers

- Tax-Deductible Contributions

Employers who contribute to their employees’ 401(k) plans can deduct those contributions as a business expense. This reduces the company’s taxable income, which can be especially advantageous for small and medium-sized businesses.

- Tax Credits for Plan Startup Costs

Under the SECURE Act, small businesses can receive tax credits to offset the costs of starting a 401(k) plan. These credits cover up to $5,000 annually for three years, plus an additional $500 annually if the plan includes automatic enrollment. This makes offering a 401(k) not only beneficial for employees but also cost-effective for employers.

- Attracting and Retaining Talent

While not a direct tax benefit, offering a 401(k) can help employers attract and retain top talent, reducing turnover costs. Many employers also voluntarily offer to match the contributions of their employees, which is essentially free money.

For example, let’s say you contribute US$5,000 and your employer matches 50% of contributions up to 100% of your salary, contributing this amount ensures you’re not leaving money, and potential tax-advantaged growth on the table. High employee retention contributes to business stability, which indirectly affects a company’s bottom line.

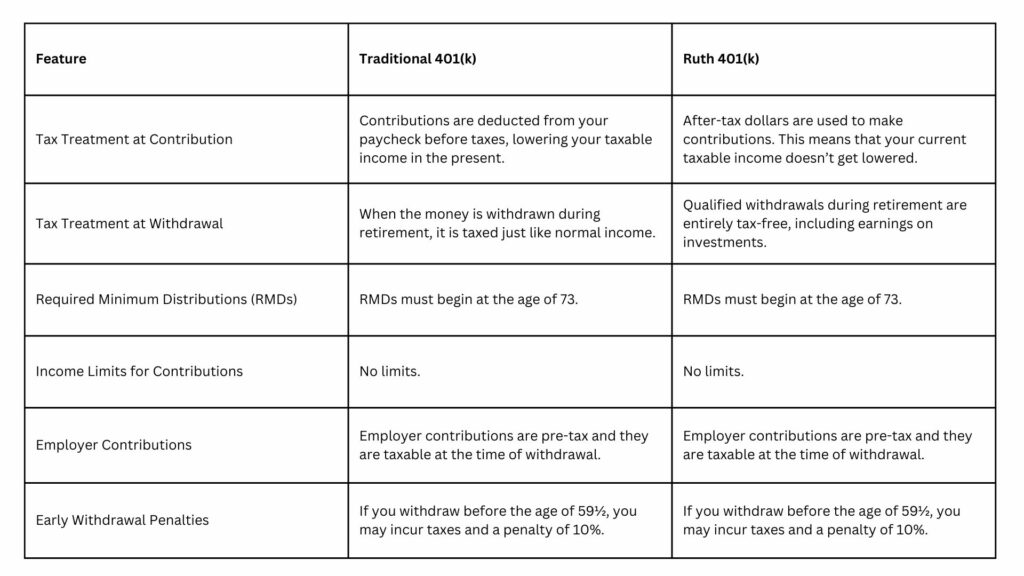

Differences Between Traditional and Roth 401(k) Plans

Choosing between a Traditional and Roth 401(k) is an important decision as it can impact your financial future and the differences will help you plan your retirement effectively. The main difference between these retirement savings plans is how they are taxed.

People often get confused while deciding between lowering their current taxable income (Traditional) and enjoying tax-free income in retirement (Roth).

Understanding the differences between Traditional and Roth 401(k) plans is crucial for determining how they impact your taxes and which one you want to pick for yourself:

Both options have their advantages, and many employees choose to diversify by contributing to both types of accounts if their employer allows.

Recent and Upcoming Changes to 401(k) Plans

The SECURE 2.0 Act is the law responsible for improving retirement savings plans like the 401(k). It has introduced significant changes aimed at making 401(k) plans more accessible and beneficial:

Increased Contribution Limits

The contribution limits have increased in 2024. The maximum amount an employee could contribute in 2023 was $22,500 and it is $23,000 in 2024. This limit will be increased to $23,500 in 2025.

For people who are 50 years or older, an additional contribution of up to $7,500 is allowed in 2024, which is the same as 2023. This limit will be continued in 2025.

Moreover, people who are 60-63 years old and participate in these plans will get a higher limit for catch-up contributions under SECURE 2.0. They will be able to contribute an additional amount of up to $11,250 in 2025.

Automatic Enrollment

New plans starting from 2025 will now be required to automatically enroll eligible employees, although employees can opt out. This ensures more individuals benefit from tax-advantaged savings.

These changes make it more important than ever to stay informed and adjust your retirement strategy accordingly.

Conclusion

A 401(k) plan is more than just a retirement savings account—it’s a powerful tool for reducing taxes. For employees, it lowers taxable income, enables tax-deferred or tax-free growth, and offers significant long-term benefits. Employers, too, stand to gain through tax deductions and credits while developing employee loyalty.

To understand the implications of 401k in more detail, contact GJM & Co. We offer you comprehensive services related to Taxation, accounting and bookkeeping, payroll accounting, payroll management, Business Formation, Virtual CFO, and more. For more, schedule a call or email us at info@gjmco.com.